Debunking KFF’s Premium Increase Canard

Chris Jacobs’s Wall Street Journal op-ed exposes a false claim of Obamacare plan premiums doubling if Biden’s COVID credits expire. This claim emerged based on a misleading and inaccurate KFF piece, as Chris documents. KFF’s argument is flawed in three ways: it ignores the continuing federal subsidies most enrollees will receive, exaggerates the impact on households, and conflates total premiums with out-of-pocket payments. Chris highlights a previous KFF analysis that found the enhanced subsidies covered an average of 88 percent of overall premiums in 2024, compared to 78 percent if the enhanced credits ended. Chris cites an Urban Institute study that households with incomes below 250 percent of the poverty level—who receive the richest subsidies and represent roughly three-quarters of all exchange enrollees—would see premiums rise only about $62.50 a month.

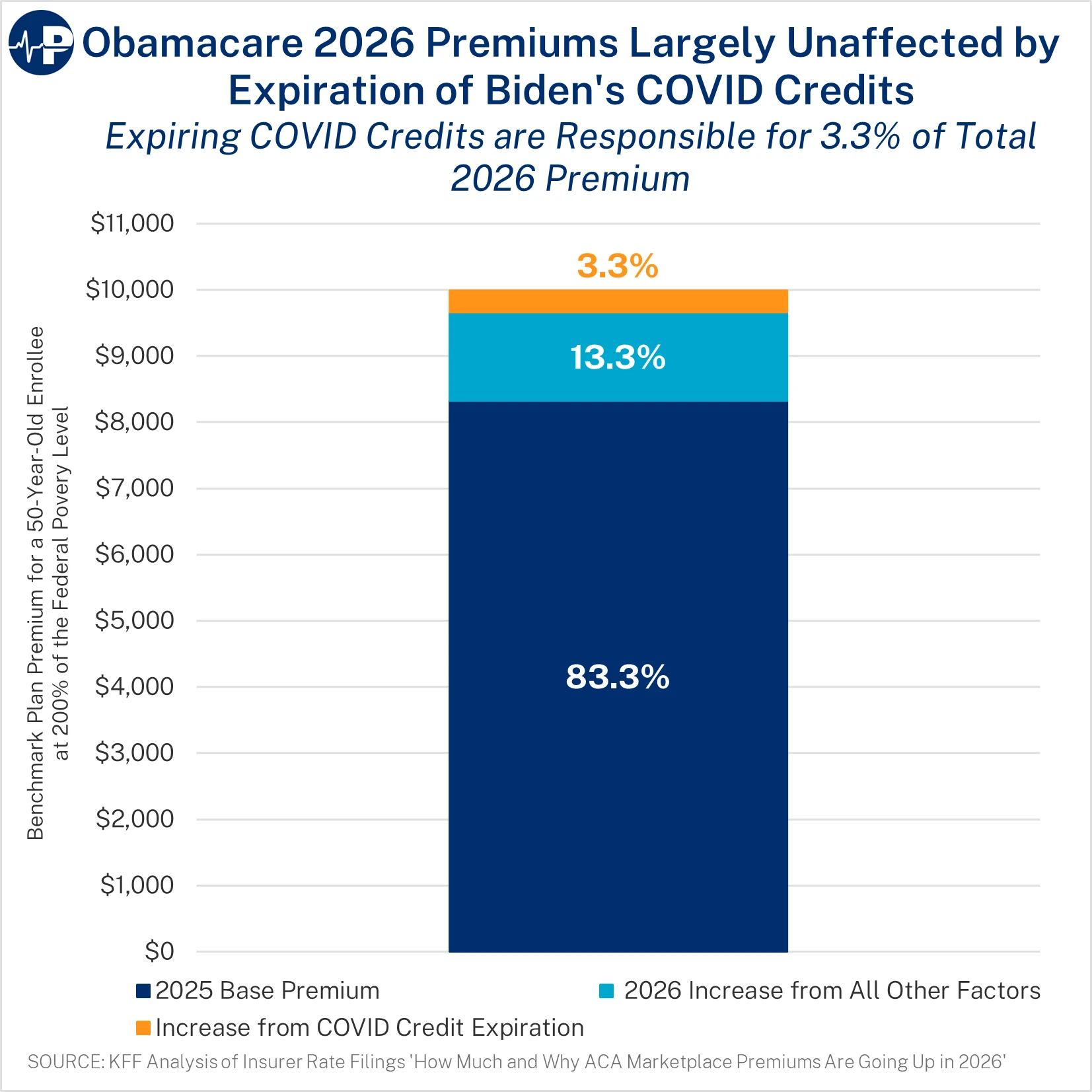

Only 3.3 Percent of 2026 Obamacare Premium is from Expiring COVID Credits

This week’s Paragon Pic shows 96.7 percent of 2026 Obamacare premiums are unrelated to the expiring COVID credits.

Insurer filings show that just 4 percent of the projected 20 percent premium increase for 2026 stems from the COVID credits’ expiration. The main causes are structural flaws in Obamacare and surging medical costs tied to inflation, consolidation, and expensive new drugs like GLP-1s. The enhanced subsidies temporarily masked these problems by inflating enrollment with zero-claim and ineligible individuals, creating the illusion of affordability. Their expiration simply exposes the underlying weaknesses of the law—not a sudden or catastrophic loss of assistance.

Brian Blase is the President of the Paragon Health Institute.