|

Last night, Congress failed to pass a seven-week continuing resolution, triggering a federal government shutdown. Senate Democrats refused to support the “clean” CR, insisting on $1.5 trillion in additional spending, including massive subsidies to health insurers, as a condition for keeping the government open.

As I discussed last week, the Democrats’ plan would repeal all the health policy provisions in the One Big Beautiful Bill, including policies that (1) restrict subsidies to U.S. citizens and certain legal immigrants, (2) require work for able-bodied adults on Medicaid, and (3) reduce Medicaid’s money-laundering schemes that result in corporate welfare. Their core demand is to continue a Biden COVID-era policy of $40 billion in additional annual federal payments directly to health insurers selling Obamacare plans above and beyond the original Obamacare subsidies that flow straight to insurers. This is despite overwhelming evidence that much of this spending is lost to fraud and does not translate into any health care received by more than one-third of enrollees.

In today’s newsletter, I discuss two prominent op-eds on why Biden’s COVID credits should expire. I then highlight a new Paragon policy brief that shows there are far more enrollees who do not use any health care compared to the number of people who would supposedly lose coverage when the COVID credits expire. I conclude with an editorial in The Wall Street Journal showing significant attrition in employer-based health coverage over the past few years—attrition driven by the COVID credits.

Ge Bai: Let the COVID Credits Expire

In a new Wall Street Journal op-ed, Johns Hopkins professor and Paragon advisor Ge Bai argues that Biden’s COVID credits must expire:

Letting the subsidies go away merely restores the original ObamaCare premium-support structure. That preserves access to subsidies for low-income populations, who already comprise 93% of the 24 million who get health insurance through the ObamaCare exchanges.

As I have written in a recent policy brief, the government would subsidize more than 80 percent of the premium for the average enrollee after the COVID credits expire.

In her op-ed, Ge explains that “since 2021, Congress has been bribing higher-income Americans to purchase expensive ObamaCare plans by hiding the plans’ true price tags using taxpayer dollars.” This is because the COVID credits raised the cap on subsidies that existed at four times the federal poverty level.

Ge documents Obamacare’s problems: soaring premiums, deductibles over $5,000, and one in five medical claims denied. In essence, these plans are so unappealing that massive subsidies are needed to get people to enroll. Those subsidies now exceed $130 billion annually. Policymakers should avoid wasting additional funds by propping up this inefficient structure with ever-larger subsidies. Instead, as Ge suggests, they should begin by asking the more fundamental question: why are Obamacare plans so unaffordable in the first place? Here’s Ge’s answer:

The inflationary provisions of the Affordable Care Act—such as the medical loss ratio, mandated “essential” benefits, community rating and premium subsidies—have inhibited insurers from offering affordable and flexible options. The law’s regulatory burdens on providers have also fueled consolidation and driven up service prices.

More from Ge, including a mention of fraud, which I discuss below:

By luring people to these expensive plans and making them dependent on subsidies, lawmakers not only wasted taxpayer dollars and invited fraud but also effectively killed the market for affordable alternatives. Continuing this scheme would be fiscally reckless and irresponsible to consumers. Covid-era subsidies should be allowed to die a natural death.

Ge then discusses how the COVID credits make health coverage worse for Americans:

By masking the true price of ObamaCare plans, Covid-era premium subsidies have distorted insurance markets and trapped people in plans they don’t want. As Americans start to understand how expensive these plans really are, they will begin demanding genuine insurance that covers only major events at affordable premiums. Innovative options—such as direct primary and specialty care, association plans, health-share ministries, and crowd-sharing arrangements—will emerge organically.

Rep. Burlison: Let the COVID Credits Expire

Congressman Eric Burlison of Missouri had a Washington Examiner op-ed on why the COVID credits should expire. According to Rep. Burlison:

42% of Obamacare enrollees are on fully subsidized plans as of 2024. Another 28% pay a premium of $50 or less. When Biden’s subsidies expire, the average enrollee (someone earning 200 percent of the federal poverty level) will only have to pay $32 a week for a plan — about the cost of a median DoorDash order. Someone earning 100% of the poverty level would only have to pay $3.45 — the cost for a cup of coffee.

Even without Biden’s COVID subsidies, taxpayers will still cover 80% of the typical enrollee’s premium —up from 68% in 2014. That’s because Obamacare subsidies cap what enrollees pay, fully insulating them from rising healthcare costs and shifting costs directly onto taxpayers.

If Republicans cave to the Left’s demands, it will be entirely clear that generous taxpayer-funded pandemic healthcare subsidies will be here to stay; almost four million Americans will lose their employer coverage, crowded out by artificially low government-backed premiums.

New Policy Brief on Zero-Claim Obamacare Enrollees by State

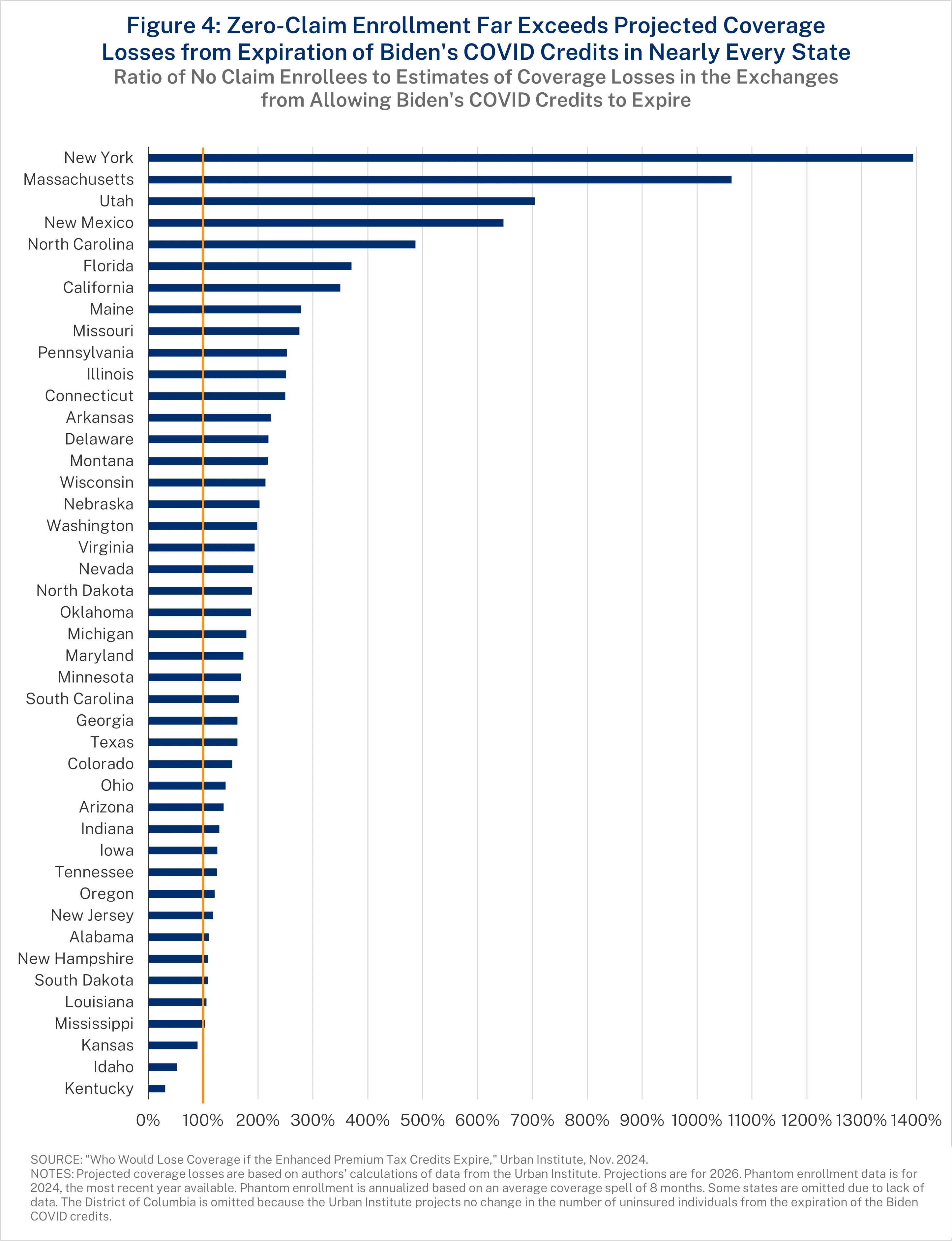

As a result of Biden’s COVID credits, there was a surge in enrollees with coverage who received no care. In fact, two in five enrollees in fully subsidized Obamacare plans did not use their coverage at all in 2024—not for a single doctor visit, test, or prescription.

In a new policy brief from Paragon, Niklas Kleinworth, John R. Graham, and Liam Sigaud uncover how these zero-claim enrollees cannot be explained by a surge of young, healthy enrollees without health care needs. The increase in zero-claim enrollees between 2021 and 2024 is more than double the increase in enrollees under 35 years of age. Rather, many of these enrollees are phantoms—people unaware of their coverage or enrolled in other plans.

Paragon estimates that more than 6.4 million individuals were fraudulently enrolled in exchange plans during 2025. These are people who claimed incomes between 100 and 150 percent of the federal poverty level to qualify for a fully subsidized 94% actuarial value plan, even though they did not earn that income. They found a very strong positive correlation between zero-claim and fraudulent enrollees by state (a correlation coefficient of 0.67). Of the top 20 states with zero-claim enrollees, 15 of them also ranked in the top 20 for fraudulent enrollment.

The large number of zero-claim enrollees severely undercuts the argument that permitting the COVID credits to expire will harm Americans’ health. Prior work from Paragon highlighted how health coverage does not translate to improved health, but those who are unaware of even having this coverage in the first place certainly would not face any negative health effect from losing coverage.

The new brief compares state projections of the increase in the uninsured if the COVID credits expire with zero claim enrollees. In all but three states, there are more zero claim enrollees (on an annualized basis) than enrollees who would lose coverage. As the figure below shows, zero-claim enrollees outnumber projected coverage losses by more than two-to-one in 17 states.

Though not all disenrollments will involve phantom enrollees, most coverage losses will likely come from people who valued coverage so little they enrolled only because it was free, or from individuals who were unknowingly enrolled by fraudsters, unaware they had ACA coverage entirely.

COVID Credits Hammering Employer Coverage

In a September 29 editorial, The Wall Street Journal reviews data from the Bureau of Labor Statistics (BLS) and highlights a massive drop in the percentage of employees covered by their employers’ health insurance plan. According to The Journal’s analysis, “the share of workers with access to medical benefits increased to 74% this year from 71% in 2019.”

At the same time, “the share of workers who participate in employer medical plans…has fallen to 65% from 73%.” The drop is steepest among lower-income workers: “part-time workers (to 44% from 56%) and employees whose wages are in the bottom 25% (49% from 61%) and 10% (34% from 57%).”

The editorial asks why—and reaches the right conclusion. “Perhaps because they can now get ObamaCare plans at no cost.”

The COVID credits were massive new subsidies—but only for people who do not have employer-based health coverage. As a result, there is less incentive for workers to enroll in employer coverage or seek employers who offer coverage. The editorial concludes: “The BLS report shows that many workers could get employer coverage if the enhanced subsidies lapse… Don’t believe the Democrats’ ObamaCare scare.”

|